An awful lot of ink has been used to comment on Britain’s fiscal rules so it’s hard not to sound like a broken record, but Reeves’ new rules aren’t much better.

If you haven’t been able to tell by the hyperlinks, I’ve been writing this piece for quite a while now. It was originally designed to be ‘response’ to the budget announcement and the corresponding rise in yields. While this is something I have already commented on, todays article aims to capitalise on the recent yield bonanza while also giving me opportunity to expand my position related to more technocratic ways of debt management.

First and foremost I would like to present to readers the chartalist view of money which posits that money derives its value from the requirement to pay taxes in the units of the specified currency. Should one try to avoid this system, the state can deploy its monopoly of violence on you, the citizen (so make sure you pay up).

Many therefore argue that a citizen's right to vote is an essential component of democracy as it ensures that tax and spending decisions align closer to the will of the people. This represents a necessary exchange of power between these two groups.

However, another group —bondholders and investors— remain largely overlooked by chartist literature. They demand money for a completely different reason than the average citizen: profit.

This difference gives bondholders the power to exert their will unto governments. They did so with Truss, and they did so quite quickly - certainly much more rapidly than the electorate or opposing party ever could - financial markets are efficient, instant. Unlike voters, they do not derive their power from electoral cycles. They mobilise their will instantly.

Thus, this creates a problem for the government. On one hand, taxpayers want to maximise their value for money which means less money going into the pockets of bondholders and more going to them. On the other hand, bondholders would prefer fatter balance sheets, which means austerity policies. This fundamental conflict of interest, paired with the differences in the speed at which these groups influence tax and spending decisions, leaves the government facing the complications of handling the opposing demands of both parties.

One could solve this problem by going balls-to-the-wall with Modern Monetary Theory (MMT) and just simply getting rid of investors. While I am somewhat sympathetic to the possibility of this working (strong emphasis), it is very radical and looks like another article idea for the pipeline.

I’d rather suggest that the Treasury shouldn’t bear the burden of catering to these two groups. Instead, there should be an independent body that the Treasury indemnifies that has the power to issue debt and by implication, decide the gross level of fiscal expenditure and corresponding optimal level of tax receipts within the economy. Did you really think my next suggestion was going to be any less radical?

I propose that this body is a merger between the Office for Budget Responsibility (OBR) and the Debt Management Office (DMO). OBR because we need an ample supply of wonks for our new technocratic fiscal overlords and DMO because we need people who know how to write up gilt contracts properly (among many other things).

All of this sounds very authoritarian. Perhaps my recent reading of Plato’s The Republic, has rubbed off on me. Nonetheless, I still lean towards the view that the optimisation of gross tax, spending, and borrowing bills should be determined by an independent and technocratic body with decisions concerning distribution being left to the matters of democracy and state. I will now argue why.

First, government expenditure does not even grow the economy that much. Fiscal decisions mostly impact the distribution of resources in the economy rather than the whole pie that goes around to the taxpayer. The only time when government spending has a significant effect on growth is during recessions where larger output gaps increase the multiplier. This gives us two conclusions. The first is that one could put in place mechanical rules where spending and borrowing decisions are approved based on their expected multiplier. The second is that what voters are voting for most of the time is how fiscal decisions should be distributed.

Second, the current regime is not and has not been beneficial for the taxpayer. The average lifetime of fiscal rules of 2 years makes me question their legitimacy and whether they respond more to election cycles rather than market signals or even economic fundamentals. Austerity leaves a sour taste in one's mouth, but I bet it tastes even more sour if I were to tell you that it was completely pointless.

Ex-IMF Research Director and MIT professor, Olivier Blanchard, makes the case that when real interest rates are below real growth rates, governments can increase borrowing and sustain primary deficits; the difference between government revenues and spending, excluding interest payments. Effectively, this is because the government can ‘outgrow’ the debt, which allows them to issue new debt to pay off existing interest payments in case creditors come knocking at their door. TLDR; when r<g, borrow, when r>g, don’t borrow.

Those who have read the literature will know the horrible reveal that the post-GFC austerity years were ones where real interest rates were below real growth rates (see chart below). In other words, not only did we not need austerity, but we could have actually spent and borrowed more throughout the 2010s (thanks, George Osborne). But those were fiscal rules of governments come and gone. How are Reeves’ rules doing? Especially in lieu of recent events, not great. Reeves’ Public Sector Net Wealth rule is okay as it has reframed political discussion surrounding investment. While financial markets don’t care about these optics - I’d be pressed to believe that investors have only just figured out that government spending creates ‘stuff’ - it does mean that Parliament may start passing bills that actually invest in the economy and that’s better than nothing. I’m still waiting on all that promised planning reform though…

But those were fiscal rules of governments come and gone. How are Reeves’ rules doing? Especially in lieu of recent events, not great. Reeves’ Public Sector Net Wealth rule is okay as it has reframed political discussion surrounding investment. While financial markets don’t care about these optics - I’d be pressed to believe that investors have only just figured out that government spending creates ‘stuff’ - it does mean that Parliament may start passing bills that actually invest in the economy and that’s better than nothing. I’m still waiting on all that promised planning reform though…

However, the first rule is what I have a real problem with. That is, balancing the current balance by 2029 - 2030 as it fails to consider the changing tides associated with Blanchard’s r<g condition which is burdening the taxpayer with unnecessary costs.

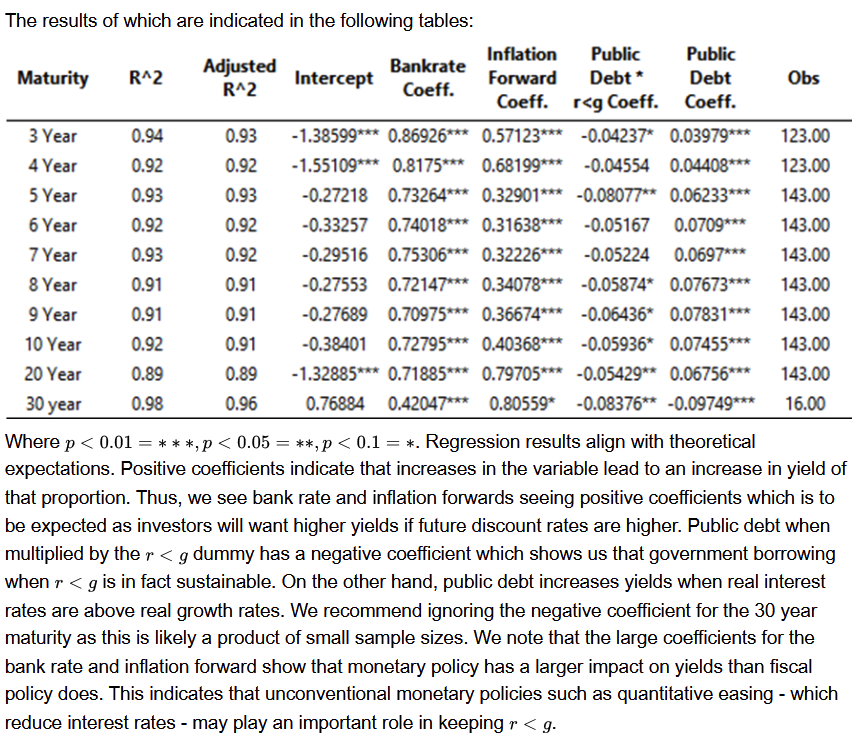

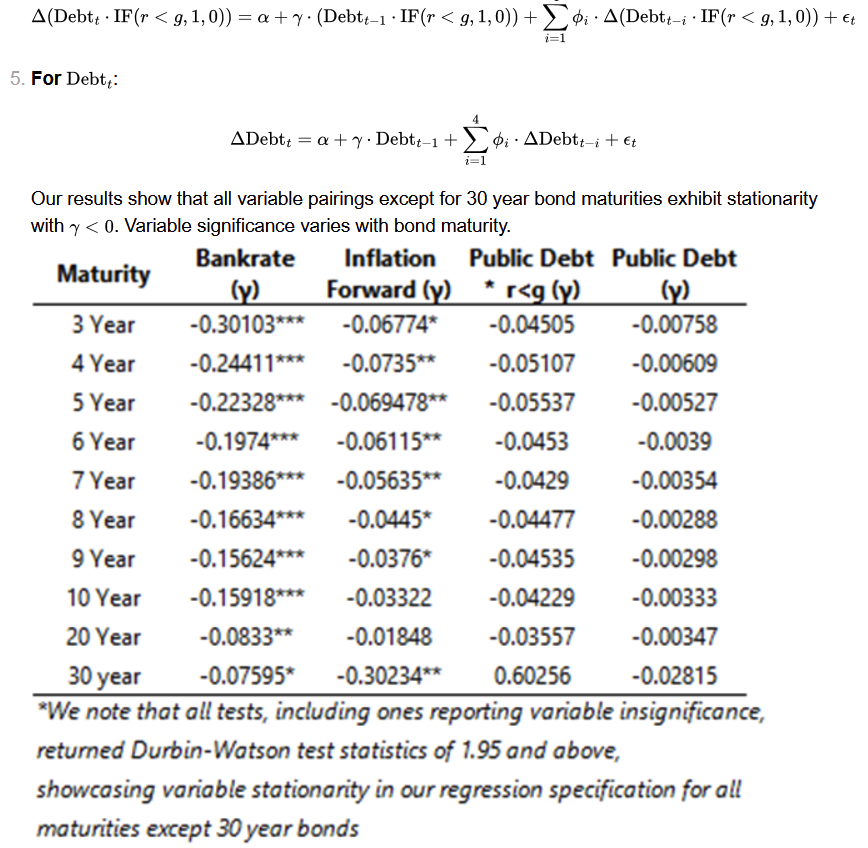

To understand why, we must first note that my previous chart indicated that we live in a world where real interest rates are above real growth rates and so any additional borrowing will cost a pretty penny. Empirically, this result is corroborated by our internal models which show that when r>g we see higher yields and vice versa when r<g (see Appendix).

I hope that at this point you have a minimal amount of faith left in the government’s fiscal credibility and that as a consequence, you have warmed up to the idea of fiscal policy being dictated by a group of technocrats who know their stuff. I hope that the mechanistic nature of the multiplier effect, and that of Blanchard’s r<g rule shows that one can determine the optimal path as well as composition (which maturities we issue) of government debt based on inflation, GDP, and interest rate forecasts. I also hope that you agree with me that financial markets are more likely to trust an independent body - whose job is to liaise and monitor them closely - rather than politicians who can cook up explosive mini budgets.

In summary, these are the logical arguments for an independent OBR-DMO merger. Before closing out this long article, I will briefly talk about how this may look, function, and some problems.

As mentioned, I think there should be an indemnity between this hypothetical institution and the Treasury. Effectively, while the OBR-DMO merger can issue as many gilts as it likes following its models, it cannot actively cut spending or raise taxes. Therefore, this institution will always run at a loss, and it will be the responsibility of the Treasury - and by extension the government - to find the money to pay for this loss by tinkering with the level or distribution of either taxes and spending within the economy.

The institution would have a dual mandate. The first would be to issue debt in accordance with r<g to maximise the amount of money that can be used on productive spending rather than just paying off the tax bill. The second mandate would be one of supporting macroeconomic stability, effectively, the institution can break the first rule in extreme cases where not doing so would threaten the stability of the entire economy.

The institution will build an array of what I call ‘just-in-case’ borrowing scenarios that kick in if financial markets freak out and we see large swings in yields. This is so that investors have some forward guidance on the direction of gilt issuance. This will assist in reducing the frequency of large swings (sunspot equilibrium) in yields, making it much easier to forecast yield paths and whether or not borrowing will be within the rule of r<g.

Mechanically, an independent institution will meet on a more frequent basis, making fiscal policy more responsive to changes in both market pricing and the macro environment. Rather than issuing budgets and changing rules whenever the Chancellor likes, monthly meetings will optimise borrowing decisions to the benefit of both the taxpayer and the bondholder.

Now time for the counter-arguments which will be kept quite short but will still hopefully elicit some discussion. Our methodology relies on the idea that there is some ‘ideal’ level of fiscal policy that is sustainable. That is, a level that reacts to the r<g condition, but when we look at it this way, we see that macroeconomic theory is not really prepared for such an idea. In the long-run, the real rate of interest converges to NAIRU, which, in current macroeconomics, is seen as something that central banks target and react to.

In other words, because fiscal policy itself can determine and affect the level of NAIRU, and by implication the supply driven growth rate of the economy, limiting fiscal policy by our r<g condition may cause more harm than good, or, can push us towards fiscal dominance where the central bank instead plays a reactionary role to the fiscal stance. Hence, because modern macroeconomics doesn’t have a ‘natural rate’ or ‘equilibrium’ rate for fiscal policy, we don’t actually know what the ‘gross’ debt issuance amount should be beyond looking at Blanchard’s condition, making it difficult for technocratic policymakers to know whether they should ‘tighten’ or ‘loosen’ the stance.

This is one of my more crackpot ideas. Discussion is always welcome. Email me your thoughts, kucharskihubert172@gmail.com

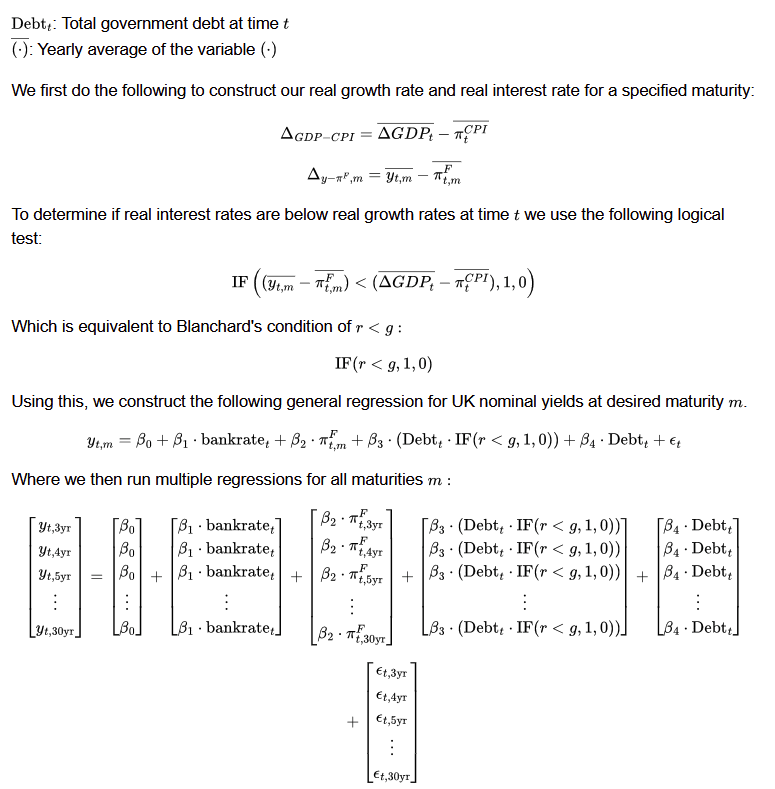

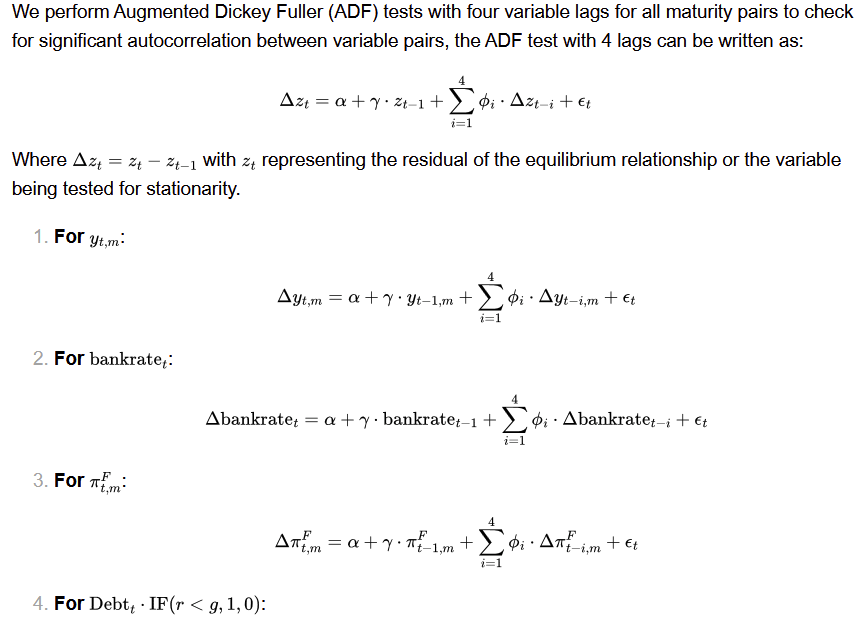

Appendix: