Bond vigilantes are unpredictable. At best, markets accurately price risk and send signals to hasty governments. At worst, they add to the social cost of bad government policy.

This was my opener for a letter to Toby Nangle’s FT article on bond vigilantes. I thought it was quite clever, but there were no responses from the pink pages this time. Unfortunately, I have a writer's itch to scratch (and that involves shamelessly repurposing this letter into a full article).

So far, it looks like targeting public sector net financial stability (PSNFL) has come out on top and is expected to give Reeves an additional £50bn every year of borrowing space for greater spending.

This rule is a mere accounting exercise. This ‘extra’ £50bn must come from somewhere and I’d pressed to believe that bondholders have only just figured out that governments accumulate assets.

Economic fundamentals dictate that debt sustainability depends on whether economic growth is higher than interest rates (in real terms). If this condition is true, governments can issue additional debt to meet their existing obligations. When false, the economy's growth is not enough to keep pace with the accumulating interest costs on debt.

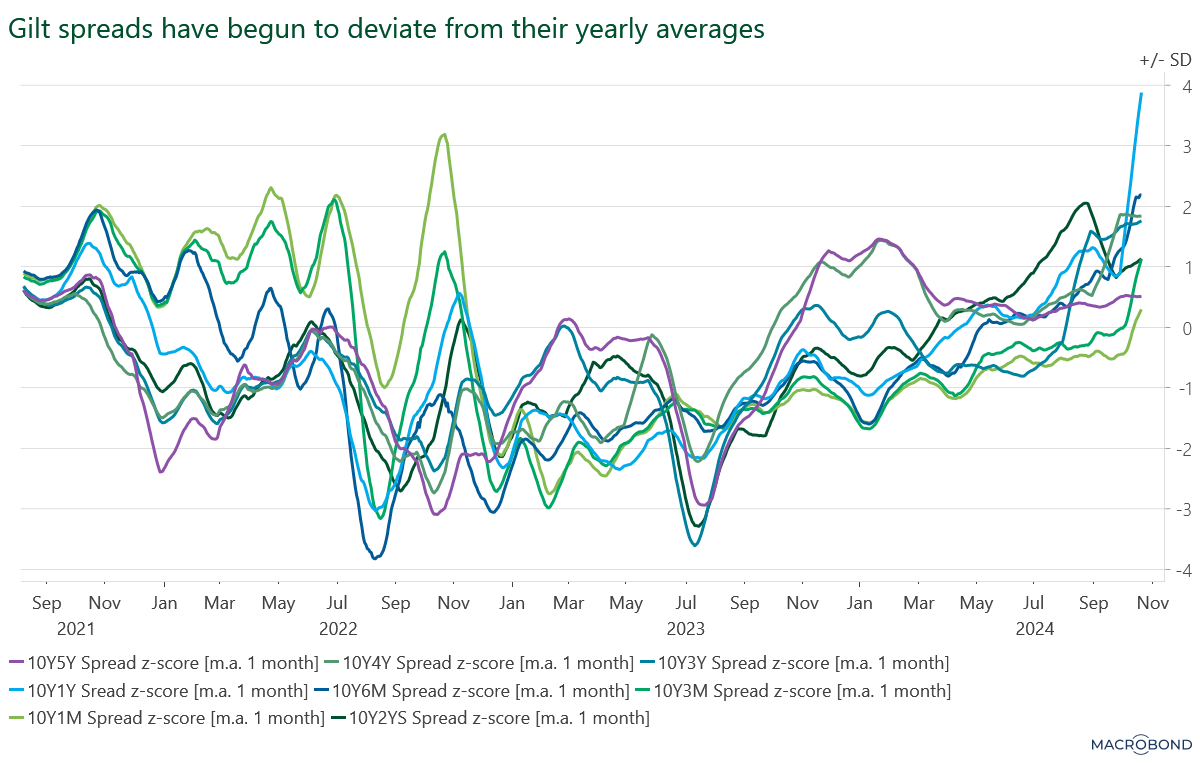

This is the key point. Financial markets know how to count. They know that we live in a high-interest, low-growth world where debt issuance forces yields to climb (see below):

Of course, these movements are natural. There is no reason to sound the Truss alarm, but Reeves’ rules certainly don’t insure us against a repeat.

Proper fiscal rules would prevent unnecessary doom loop spirals in gilt yields. The best prescription for this is through the help of the good people at the OBR via Just in Case Budgets (JiBs). JiBs involve pairing each budget with a corresponding emergency budget that only kicks in if and only if yields exceed levels that would pose financial stability risk.

Their role is to guarantee investors a payout even when fiscal conditions become constrained. In doing so, they remove speculative fears over fiscal sustainability thereby preventing gyrations in yields that are detached from economic fundamentals.

But how do we figure out when gyrations pose financial stability risk? Well, fortunately for you dear reader, I have an answer. Unfortunately for me, this involved spending the majority of the last few days staring (and swearing) at my computer screen at very unsociable hours while trying to understand this stuff.

In what may be a feeble effort to keep this article as readable as possible, I have banished technical jargon to the bottomless known as the appendix. Note, this does not insure this piece against the use of financial market gobbledygook, we all have to start somewhere.

My start was a mathematical model to see how certain factors affected 10-year yields on a 90-day rolling basis detailed in the appendix, for the econometricians amongst you. For the non-technical reader, I simply estimate how the yield (or expected return) of 10-year UK 'gilts' (or bonds) are affected by a series of variables, namely:

(1) the Sterling Overnight Index Average (SONIA), - which functions as an interest rate benchmark; (2) implied (expected) inflation; (3) changes in repo (a way for financial institutions to borrow money short-term by selling assets (like government bonds) with an agreement to repurchase them later) usage; and (4) the forward/spot spread on SONIA (a way to measure what people think will happen to interest rates in the future compared to safe investments, like government bonds).

(1) and (2) are pretty straightforward as we use these to model our medium to long-term path for yields. If you need a primer on bond pricing, I recommend the following FT piece but one key thing to remember is this: bond pricing and yields are inversely related.

If you are still here, the other two variables are what we will use for measuring market stress as this should work as a good proxy for the impact of unique events like terrible budgets. In the case of repo usage, one would expect an increase during acute stress periods where liquidity is low. Meanwhile, we can infer an elevated uncertainty or risk aversion in the market when forward rates significantly diverge from spot rates, as investors demand compensation for potential future volatility.

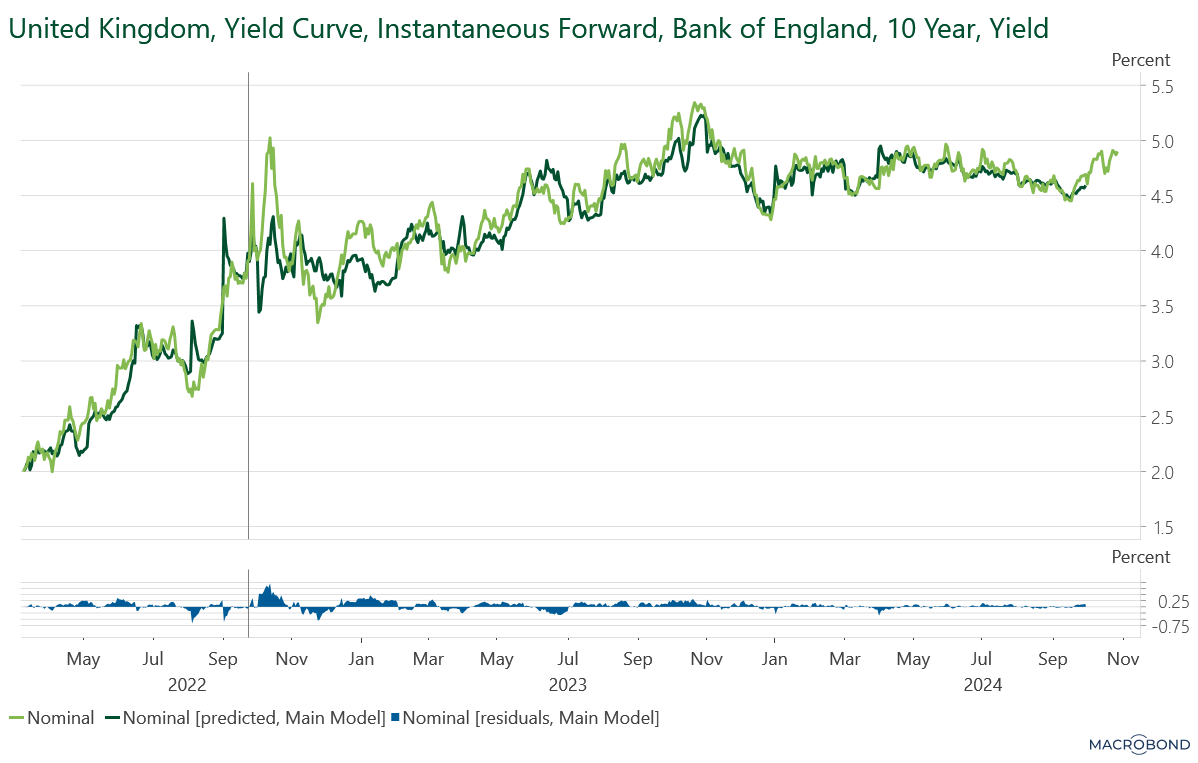

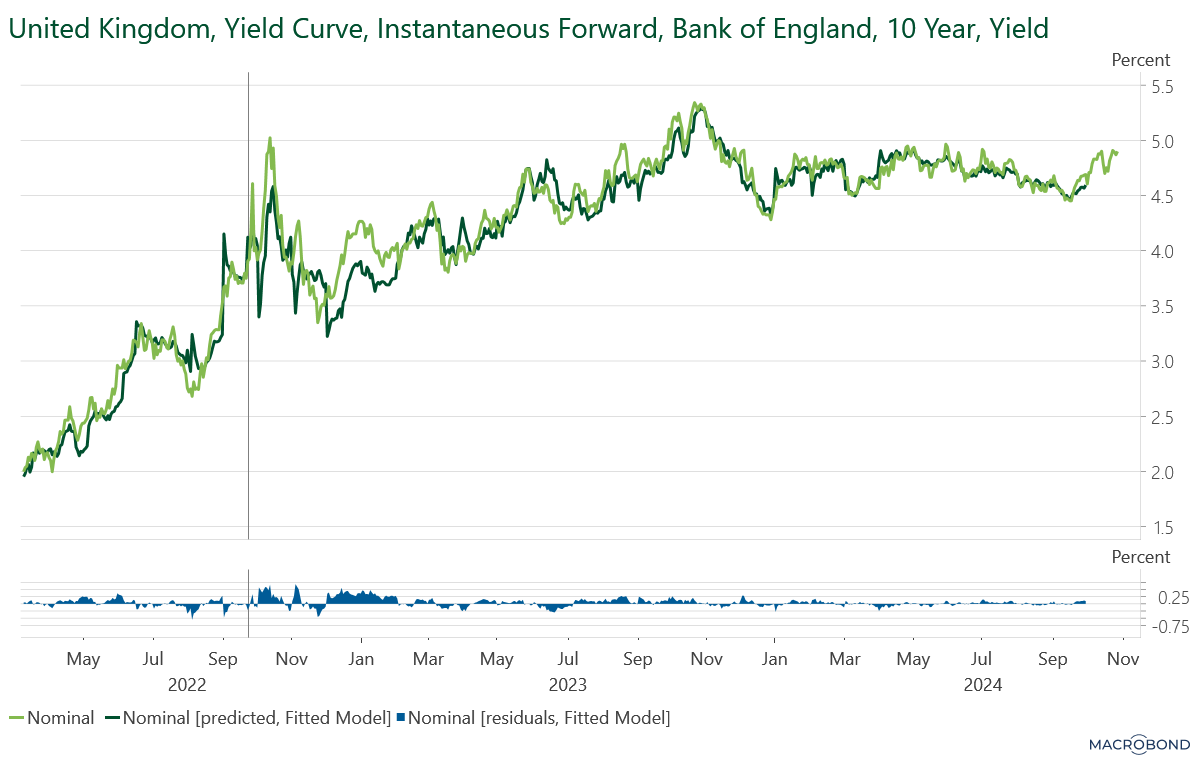

Now that we got that out of the way, let's look at how good our model is:

Decent. The model is not perfect at mapping the Truss episode but at least it did estimate an increase in yields. This gets us a lot closer towards constructing a measure of market volatility to avoid future financial stability risk.

To get to this stage, we need to figure out if changes in our estimators are down to increases in market volatility or changes in the underlying relationship between bond yields and our variable of interest. While this sounds tricky, it is quite easy to do as we can use the following formula for calculating estimators:

I won't go too deep into the notation, but in words, this equation means that our regression slope for a specific variable can be calculated by multiplying the correlation coefficient between the dependent variable and the variable of interest by a ‘variance factor.’ The variance factor is a measure of the relative volatility, or variability, between variables in our regression model. Specifically, it compares the standard deviation of the dependent variable to the standard deviation of an independent variable, X.

Increases in the variance factor show that the predictive power of a variable is not down to a better causal fit brought by a better correlation coefficient but instead by greater variance. In the case of rolling regressions, this means that the variance factor can grow for variables that have no causal link with stress periods as the increase in the standard deviation of Y must be compensated by growth in the estimator.

In the case of the Truss episode, we would expect this variance factor to grow in line with the correlation coefficient of our market-stress variables as this would represent a causal relationship that plays into more volatile market conditions. Fortunately, this is exactly what the decomposition shows:

In fact, it is possible to fit this model even more towards the Truss episode by adding total repo usage to our regression specification. When doing so, we see the following results:

Much better. As we can see, in both cases, the variance factor and correlation coefficients for our market stress variables increase after the 23rd of September, the date of the mini-budget announcement.

To say that this model has managed to decompose these effects using publicly available data via Macrobond makes this research extremely valuable as one can use this variance factor as a proxy for market sentiment. Current research on the Truss episode has mainly come from the Bank of England and through the use of privileged datasets.

Going forward, I would like to use this modelling approach in future articles to create hypothetical scenarios where gyrations in yields are constrained by the aforementioned Just-in-Case Budgets to test whether such a policy recommendation would prevent future Trussonomics episodes. I expect they would, but that is a story for another day.

If you are interested in the data and methodologies underlying this piece - or have some interesting views on today's budget - please shoot me an email at kucharskihubert172@gmail.com

Photo by Pasi Välkkynen, under the Creative Commons Attribution-Share Alike 2.0 Generic license

Appendix: