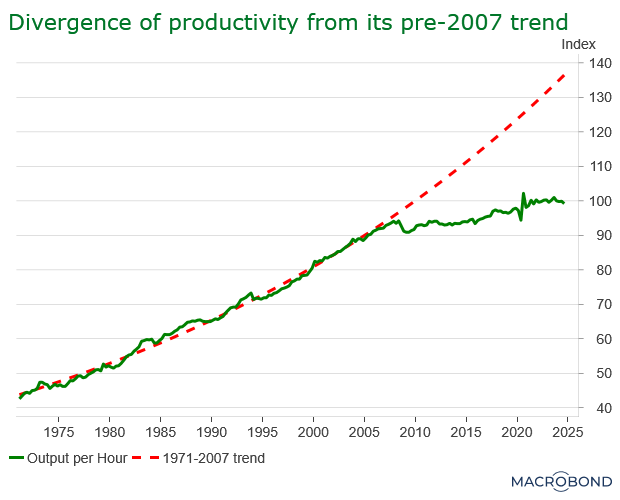

For the past few months, Labour’s rallying slogan has been very clear: this country needs economic growth. To be fair, growth is pretty great. GDP going up is usually a sign of increasing employment and productivity, making government debt more manageable due to increased tax revenues. The room to grow certainly seems to be there: as Rachel Reeves seldom fails to remind the nation, “had the UK economy grown at the average rate of OECD economies over the fourteen years from 2010, it would be £143.3bn larger”. There are similar signs for productivity: had pre-2008 trends continued, it would’ve been around 26% higher in 2022 and, from my own analysis, over 35% higher today. That would mean that on average, an hour of work for everybody in the economy would be worth 35% more. We could probably all buy ourselves a nice little holiday with that.

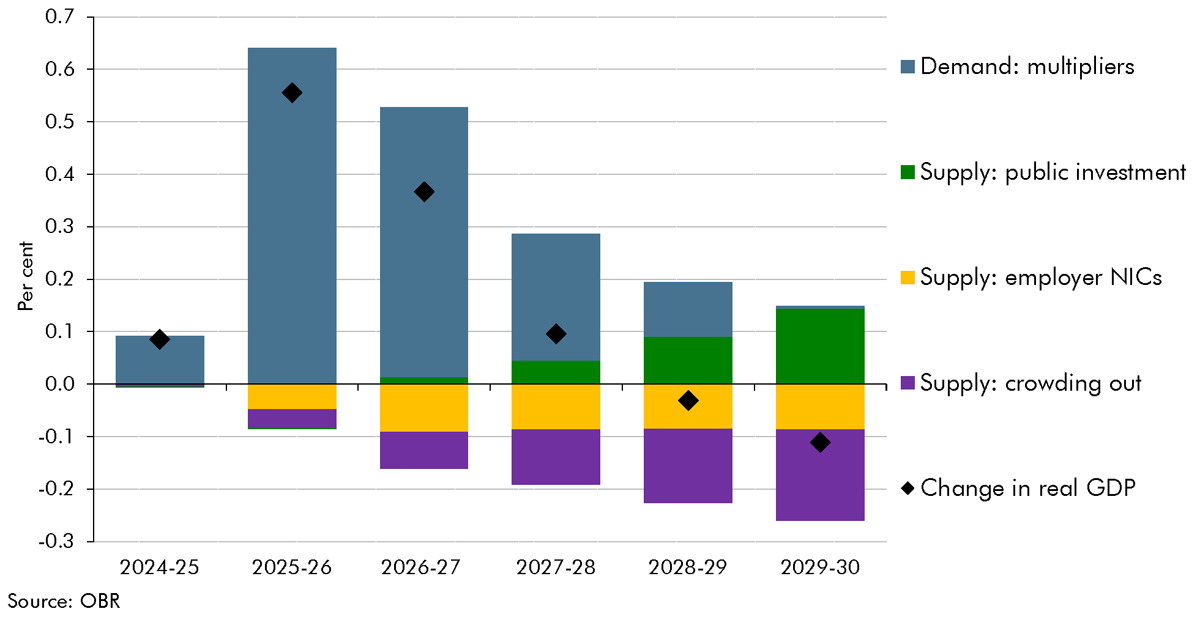

Of course, it’s one thing to acknowledge this gaping Grand Canyon of an output gap… and Labour’s plans to fix it leave some wanting. The OBR estimates that, while the Autumn budget will boost GDP over the next 4 years mainly due to increased demand, it will damage the supply-side by increasing employers’ National Insurance contributions (NICs) and crowding out the private sector; crowding out happens when interest rates rise due to government borrowing and subsequently disincentivise private investment. In total, they project a lower GDP in 2028-30 than if there were no changes at all. Interestingly, later in the report they do claim a net positive impact going into the early 2030s.

The OBR maybe missed a trick on this one. It seems to me that the Biden-Harris administration’s large public spending programs crowded in the private sector and beat expectations; considering it’s exactly that kind of government spending that Reeves wants to emulate, it could be Labour’s turn to surprise OBR economists and prove we’ve been underestimating crowding in for far too long.

As I’ve been writing this article, revised estimates show that the UK economy experienced zero growth from July to September and shrank a bit in October. While the budget will only fully come into effect in April, it seems that Reeves’ recent pessimistic monologuings combined with sustained high interest rates have tanked public confidence, freezing private sector recruitment and causing disinvestment. On the bright side, at least inflation is… hm… well we’re hoping it will get to 2% quite soon.

Setting that whole debate aside for a second, the common message from both team crowd-in and crowd-out is clearly that the country needs private investment. The effective and efficient allocation of capital to productive enterprises is, if you think about it, kind of the whole point of capitalism – it is coincidentally also one of the best ways to grow your economy. Unfortunately, it seems our tax policy is contrived in such a way as to spit in the face of “efficiency” and maybe, probably, give a giant middle finger to the concept of “effective”. At least, that’s what the IFS, a think tank, has determined after analysing the UK’s capital gains tax (CGT).

A capital gain occurs when I sell some asset at a higher value than I paid for it, i.e., a positive net profit. Some examples of taxable assets include property and company shares – however owner-occupied homes and ISAs are excluded.

The problem, pointed out by the IFS, is distortions created by CGT. A distortion happens when a firm forgoes an investment that they would have made, were it not for the presence of the tax. Obviously, we can all think of times where we want taxes to be distortionary, like carbon, sugar, and cigarette taxes. Private investment in general is definitely not in that group and discouraging it when we don’t want to is… bad. Unintended distortions happen when the projected return on investment (ROI) is reduced by the tax to such an extent as to make the investment no better than simply putting your money in a savings account. Every time this happens, we substitute potential investments like new housing or machinery with flaccid, lifeless, savings simply because of our tax structure. Even worse is this:

For a relatively low CGT, like 10%, we lose the least valuable investments – if we assume the interest earned on savings (savings rate) is 5%, then only investments with expected returns between 5%-5.56% are effectively lost. However, imagine CGT rises to 40%, matching the top rate of income tax. With the same savings rate of 5%, expected returns all the way up to 8.33% are not worth it. The economy not only misses out on a greater quantity of private investment, but greater quality – an enterprise with an 8.33% expected ROI likely has more room to grow and will contribute to the economy more than one with an expected ROI of 5.56%.

Fortunately, taxing gains is still on the table. I say fortunately, because it’s clear why – to me at least – CGT ranks highly on the list of taxes people want to raise. It doesn’t feel right that people who make money with money have their work taxed less than the rest of us. On the other hand, I’m sure most of us are feeling the burn of a stagnant economy. So, let’s modify CGT to ensure efficient productive investments that help the public purse as well as the private sector, so we can have our gains and eat them too. The trick is, rather than levy CGT on the whole gain, only tax the extra gain on top of the savings rate in an economy. With a savings rate of 5%, investments with a 5% ROI wouldn’t pay CGT at all. With an 8% ROI, that surplus 3% would be taxed at whatever rate we put CGT at. Incidentally, that’s the fun part: with this system, CGT can be set as high (or as low..?) as we want, without discouraging any investment that would have happened otherwise. Taxing like this is also fairer for everyone: we can achieve parity between CGT and income tax, thereby taxing everyone’s work the same without messing with capital allocation.

The IFS report goes into more technical depth on three different methods of implementing the new system. My main takeaway, though, is this - it’s true that the past decade and a half has given us lots of space to grow - mainly due to 14 years of an elongated economic fumble rather than any great feat on our part. Instead of wondering, “what if?” I’m glad the new government has finally taken the first steps to revive tales of government stimulus coming from across the pond. However, we’re off to a shaky start - if we learn to embrace new, possibly complicated but definitely robust economics, we’ll finally stop playing catch-up and remember what it feels like to lead by example.